Maryland Uninsured Motorist Frequently Asked Questions

If you have been involved in a Maryland car accident involving an uninsured driver or underinsured driver in Maryland, you have the right to file an uninsured motorist claim, and in certain instances an underinsured motorist claim.

The personal injury lawyers at Saiontz & Kirk can help you navigate Maryland’s uninsured motorist laws and make sure you get the compensation you deserve.

Maryland Uninsured and Underinsured Motorist Info On This Page

What is Maryland uninsured motorist coverage?

What types of Maryland uninsured motorist claims can be filed?

Maryland Uninsured or Underinsured Motorist Statute of Limitations

Do I need a lawyer for a Maryland Uninsured Motorist claim?

What is Maryland uninsured motorist coverage?

Maryland is one of the few states that requires uninsured motorist coverage by law.

Uninsured motorist (UM) insurance is coverage that helps cover the damages to your vehicle, your medical expenses, lost wages, and other damages resulting from an accident caused by a third party that does not have motor vehicle insurance, and cannot cover your expenses, or if you are involved in a hit and run accident, where someone flees the scene of a motor vehicle accident and is not identified.

Uninsured motorist coverage (UM) is available from your insurance provider in addition to the liability insurance that is required by law. If you have both UM and PIP coverage, you may be able to recover much more than only having uninsured motorist coverage.

It is always a good idea to check with your insurance company and a Maryland car accident lawyer to find out exactly what your options are and how much uninsured motorist coverage you have in the event of an accident.

Maryland Uninsured Motorist Coverage Laws

Maryland law requires that all drivers maintain a minimum level of auto insurance coverage. Under section 19-509 of the Maryland Insurance Code, policyholders are required to purchase uninsured/underinsured (UM/UIM) motorist bodily injury liability insurance that covers at least;

- $30,000 in damages per person injured

- $60,000 per accident

As of October 2017, Maryland drivers now have the ability to purchase enhanced underinsured motorist (EUIM) coverage under section 19-509.1(c) of the Maryland Insurance Code.

What compensation can I receive from an uninsured driver claim?

The purpose of uninsured motorist coverage (UM) is to ensure that you have access to all available means of compensation for your Maryland auto accident, even if the person who caused the accident is driving a vehicle that is not insured, if you are a victim of a hit and run, or if the at-fault individual is for some reason excluded from the insurance policy for the vehicle they were driving.

With uninsured motorist coverage, you can make a claim to be compensated for the damages to your vehicle, the same injuries, medical treatment, lost wages, and pain and suffering as you would if the negligent driver was insured. There is no difference in the compensation allowed. The Maryland legislation enacted this so that the large insurance companies are the ones that bear the burden of uninsured motorists’ claims, and not innocent victims.

Does uninsured motorist coverage pay for pain and suffering?

Yes. The purpose of Maryland uninsured motorist coverage is to provide a means for individuals to collect compensation for damages arising from the car accident in a similar fashion to accidents caused by individuals with valid and/or sufficient car insurance. Under uninsured motorist coverage (UM), individuals are allowed to receive compensation for pain and suffering in addition to other economic damages such as medical expenses and lost wages.

Pain and suffering is a physical or emotional discomfort that one experiences as a result of an injury. It can be described as both the mental and physical anguish that someone goes through after sustaining an injury. This anguish can be short-lived, or it can last for a long time depending on the severity of the injury or the trauma associated with the injury. Placing a monetary value is subjective, but there are some factors that play into calculating a pain and suffering settlement.

What types of Maryland uninsured motorist claims can be filed?

In Maryland, there are three different kinds of uninsured motorist claims you can file; uninsured motorist (UM) and underinsured motorist (UIM), and unsatisfied claim and judgment (UCJ).

Maryland Uninsured Motorist Claim: An uninsured motorist claim can be filed when neither the person who caused the accident nor the vehicle they were operating is insured, when the insurance company for the vehicle for some reason excludes coverage for the driver operating the vehicle, or when you are the victim of a hit and run.

Maryland Underinsured Motorist Claim: An underinsured motorist claim can be filed when there is insurance coverage for the person who caused the accident or the vehicle they were operating but the limits of that coverage are low and not enough to cover the full cost of the damages you sustained from the accident. Whether you can file an Underinsured Motorist claim may also depend on your own insurance limits, but we will explain this further below.

Unsatisfied claim and judgment (UCJ): This is a claim filed with the Maryland Auto Insurance Fund (MAIF) or Maryland Auto Insurance as they like to be called now, for compensation. Maryland UCJ claims have strict rules and only offer a small amount of coverage. A UCJ claim with the Maryland uninsured motorist fund as it is sometimes referred as, should only be filed if it is you have exhausted all of your other options and if you meet the criteria set forth under Section 20-601 of the Maryland Insurance Code.

What is Underinsured Motorist Coverage?

Underinsured motorist coverage (UIM) provides protection when the at-fault party who causes the accident has liability insurance but not enough to cover the total amount of your damages, which include your medical bills, property damage, pain and suffering caused by a motor vehicle accident in Maryland.

Much like UM, Maryland law requires that all insurance companies providing private passenger motor vehicle liability policies supply UIM coverage.

An example of when you would use your underinsured motorist (UIM) coverage would be:

An in-state or out-of-state driver was at fault for your accident and does not carry enough coverage on their policy to cover the damages they caused in the accident.

You would then seek the difference from your own underinsured motorist coverage policy.

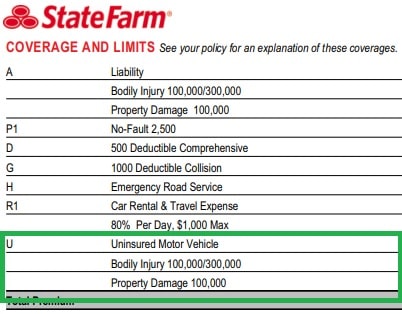

- Let’s say you carry a $200,000 underinsured motorist coverage policy with State Farm and are hit by someone resulting in $300,000 worth of damages.

- But, the underinsured driver only has a $100,000 policy.

- In this scenario, the at-fault driver’s policy would pay their $100,000, and your underinsured motorist coverage would pay out $200,000 (the difference between the at-fault party’s total limits and your total UIM policy limits).

UIM can also be used if an accident is caused by an out of state driver who has lower policy limits than required in Maryland. This can be a common occurrence as several states have lower required liability insurance limits. For example, the District of Columbia only requires that vehicles carry $25,000.00 in coverage per person and $50,000.00 per accident.

You may also want to file a UIM claim if you are involved in an accident where there are several victims and the insurance company for the at fault driver or vehicle is forced to split their policy between the victims. Your own UIM coverage may be able to make up for any difference in the value of either your property damage claim, medical expenses, or pain and suffering if you were forced to accept a lesser value as a result of the limited policy limits available

If you find yourself in one of these scenarios, it is very important that you consult with an experienced uninsured motorist Baltimore lawyer that will be able to navigate your claim through Maryland’s uninsured motorist laws. An experienced Baltimore accident lawyer will be able to make sure you get the compensation you deserve without failing to take the necessary steps of this process. There are nuances to pursuing a UIM claim including:

- Making sure that any subrogation rights held by your own insurance company are protected

- Confirming that your insurance company is allowed to make a subrogation decision as prescribed by Section 19-511 of the Maryland Insurance Code.

What is enhanced underinsured motorist coverage?

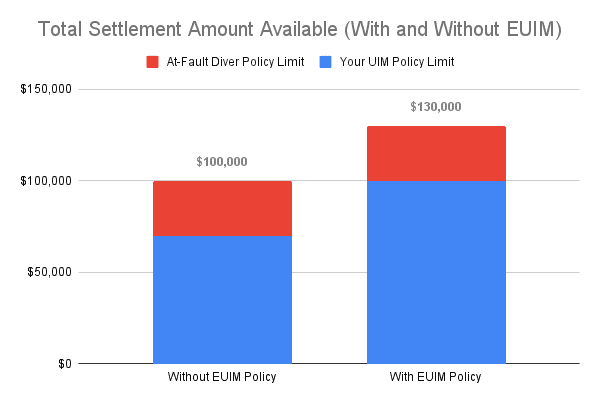

Enhanced underinsured motorist coverage (EUIM) provides the same benefits as traditional underinsured motorist (UIM) coverage with a very specific difference. Under traditional UIM coverage, the portion of the settlement your insurance company is responsible for would be reduced by the total amount of the policy limits of the at-fault vehicle. In other words, you cannot “stack” the insurance policy limits.

Traditional UIM only allows you to pursue a settlement amount up to your total UIM limits. So if your UIM limits are $100,000 and the at-fault party paid out their limits total of $30,000 then your insurance company would only be responsible for a maximum of $70,000, the difference between the at-fault party’s total limits and your total UIM policy limits.

With EUIM coverage, your policy limits can be used in total as an addition to the at-fault party’s. In other words, the policy limits can be “stacked.” Therefore, if your EUIM policy limits are $100,000 that full amount would be available on top of the at-fault party’s policy limit pay-out for a total of $130,000.

What is the Maryland Uninsured or Underinsured Motorist Statute of Limitations?

The Maryland statute of limitations for Underinsured/Uninsured motorist benefits is three (3) years. This period begins on the date the insured party would have known that there was a possible claim that could be filed with the insurance company. This is typically the date of the crash or incident leading up to the claim, but in very specific circumstances, if you are pursuing a UIM claim, the three year statute of limitations may not start running until the UIM insurance company “denies” your claim.

The Maryland Court of Appeals, or the equivalent of the State Supreme Court, recently issued a decision on the Nationwide v. Shilling case. This decision addressed the question of when the 3-year statute of limitations begins to run on a UIM claim.

The Maryland court said that a UIM claim is at its core a breach of contract action, so the statute of limitations begins to run when the insurance company breaches the contract by denying the insured’s UIM claim. This can be very confusing as insurance companies do not always distinctly deny UIM claims, therefore, there can be disagreements as to when a UIM claim is denied. Given these complications, it is very important that an experienced Baltimore uninsured motorist attorney reviews the statute of limitations on your UM or UIM claim.

Additional MD Uninsured Motorist FAQs

What Are Auto Accident Policy Limits?

Motor vehicle insurance policy limits are the maximum amounts that an insurance provider will pay to cover damages resulting from a motor vehicle accident. These limits typically apply to things like medical bills and property damage, and they are usually determined based on factors such as the severity of the accident and the history of each driver involved.

Generally speaking, car insurance provides primary coverage up to these limits in the event of a collision or other incident. However, it is important to note that policy limits may vary depending on individual circumstances, so it is crucial to consult with a Maryland car accident attorney to understand how your particular coverage works in order to protect yourself following a car crash.

Does Maryland require uninsured motorist coverage?

Yes. Maryland does require uninsured motorist coverage. This type of car insurance coverage is an essential part of any auto insurance policy in the state, as it protects drivers against accidents with uninsured or underinsured motorists.

By law, Maryland residents must maintain at least a minimum amount of this coverage, so it is important for drivers to understand exactly what kinds of benefits this policy provides and how it can help them in the event of a motor vehicle accident.

Can you waive uninsured motorist coverage in MD?

No. If you are the first named insured of a passenger (the insurance policy is in your name) and you have liability coverage, you can submit a written waiver affirming that you choose not to have uninsured motorist coverage in the same amount as your liability coverage. If that coverage is above the statutory minimum of $30k/person $60k/accident. A waiver does not remove UM coverage from your policy, it reduces it to the statutory minimum.

When can I file a Maryland uninsured motorist claim?

If you are injured by a verified uninsured driver in a Maryland auto accident, you do not have to wait to file an uninsured motorist claim, you can file one immediately. There is no minimum waiting period in order to file a Maryland uninsured motorist claim. However, it must be verified that neither the at-fault vehicle nor the driver of the at-fault are insured before that claim can be filed using your own coverage or that for the vehicle you were in.

There is a time limit on how long you have before you can no longer file a claim. A person injured in a Maryland auto accident has up to 3 years from the date of the accident to file a claim with the insurance company. This includes uninsured motorist claims.

Does filing an uninsured motorist claim raise my rates?

While it seems unfair, unfortunately, it is possible that your insurance company could raise your rates after filing an uninsured motorist claim in Maryland. Unlike the states of Oklahoma and California, Maryland does not have a law prohibiting insurance companies from raising premiums after filing an uninsured or underinsured motorist claim. Insurance companies may also say that they will not raise your rate, but they will remove certain discounts in your policy, which in turn raises your rate.

However, an increase in insurance premiums is not guaranteed. Each insurance provider has its own policies concerning this. It is best that you contact your insurance provider to get correct information about their company’s policies concerning premiums and uninsured or underinsured motorist claims.

Do I submit the uninsured motorist claim to my insurance company?

If there is a chance that either the at-fault driver or the vehicle they were driving has insurance you must attempt to file a claim with their insurance company first. You should only attempt to file an uninsured motorist claim with your insurance company after it has been verified that the at-fault vehicle and/or driver are uninsured.

Do I need to be driving my own vehicle to file an uninsured motorist claim?

No. You do not need to be driving your own vehicle to file an uninsured or underinsured motorist claim in Maryland.

If you are the passenger in someone else’s vehicle you can file under the insurance coverage for that vehicle. If you are driving someone else’s vehicle with their permission, you can also file an uninsured motorist claim under that vehicle’s coverage.

Regardless of whether you are a passenger or driver of a vehicle that is not your own you can still file the claim with your own insurance company if the insurance coverage of the vehicle you are in is less than your own coverage.

Should I Hire a Maryland Uninsured Motorist Lawyer for My UM Claim?

While you can try to negotiate a settlement after an accident with an uninsured motorist on your own, your best chance of getting the compensation you deserve for your injuries, pain and suffering is by having a trusted, experienced Maryland auto accident attorney on your side.

Even though most uninsured motorist claims are filed using your own auto insurance coverage, the fact still remains that the insurance company’s own interests are their main concern; they are not on your side. It is important to understand that you are going up against a company of seasoned professionals who are happy to give you the bare minimum in compensation for your pain and suffering caused by an uninsured motor vehicle accident.

You should have a group of experienced professionals on your side who represent your best interests. The attorneys at Saiontz and Kirk have decades of experience making sure that our clients are fully compensated for all injuries caused by a Maryland auto accident.

Contact Saiontz & Kirk For A

FREE ACCIDENT CASE EVALUATION